How you can retire with a smaller retirement: Many people dream of retirement but worry that their savings won’t be enough. The good news is that retiring comfortably doesn’t always require a massive nest egg. With smart planning, lifestyle adjustments, and a bit of creativity, you can make a smaller retirement fund work. In fact, surveys show that while Americans think they need around $1.26 million to retire comfortably in 2025, plenty live fulfilling retirements on much less by focusing on what truly matters.

kiplinger.com

kiplinger.com

Why a Smaller Fund Can Still Lead to a Happy Retirement

Traditional advice often suggests saving 10-12 times your annual salary by retirement age. But reality is more flexible. Your actual needs depend on your lifestyle, location, and health. Social Security can cover a big chunk—often 40% or more of pre-retirement income—and many retirees find their expenses drop because they no longer commute, save for retirement, or pay work-related costs.

By lowering your spending and maximizing other income sources, a nest egg of $500,000 or even less can support a comfortable life, especially if you’re debt-free.

Key Strategies to Retire with Less Savings

Here are practical ways to stretch your retirement dollars further:

- Cut Major Expenses: Downsize your home or move to a lower-cost area. Paying off your mortgage before retiring frees up thousands monthly.

- Embrace Frugal Living: Track spending and focus on free or low-cost joys like gardening, reading, or hiking.

taking.care

10 Beneficial Hobbies & Interests for Over 60s | TakingCare

- Maximize Social Security: Delay claiming until age 70 to boost benefits by up to 8% per year past full retirement age.

- Generate Side Income: Consider part-time work, renting a room, or a small hobby business to supplement your fund without full-time stress.

- Relocate Smartly: Move to affordable states or countries with lower taxes and living costs—many retirees thrive this way.

- Stay Healthy: Preventive care reduces medical bills, one of the biggest retirement expenses.

These steps can reduce your annual needs from $60,000+ to $40,000 or less, meaning a smaller fund lasts longer.

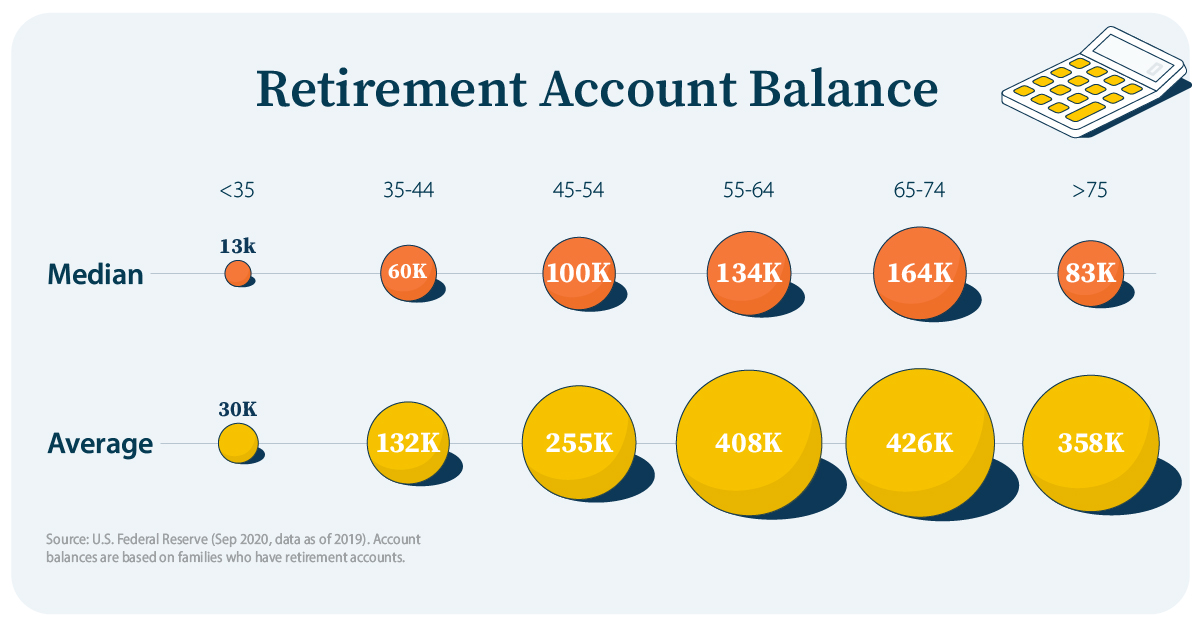

Retirement Savings Comparison Table

Here’s a quick look at benchmarks versus reality (based on 2025 data):

| Age Group | Recommended Savings (Multiple of Salary) | Average Actual Savings | Median Actual Savings |

|---|---|---|---|

| 30s | 1-2x | ~$100,000 | ~$50,000 |

| 40s | 3-4x | ~$200,000 | ~$90,000 |

| 50s | 5-7x | ~$400,000 | ~$150,000 |

| 60s | 8-10x | ~$550,000 | ~$200,000 |

advisor.visualcapitalist.com

Retirement Savings: How to Tell if You’re on Track

Even if you’re below averages, adjustments like those above can bridge the gap.

Frequently Asked Questions (FAQ)

How much do I really need to retire? It varies, but aim for 25x your annual expenses (the 4% rule). If you live on $40,000/year including Social Security, $500,000-800,000 might suffice.

Can I retire with under $500,000? Yes, especially with Social Security, a paid-off home, and modest spending. Many do it happily.

What if I’m behind on savings? Start now: Boost contributions, cut costs, and consider working longer for more growth time.

Is relocating worth it? Absolutely—lower taxes and costs in some areas can add years to your fund’s lifespan.

Conclusion

Retiring with a smaller retirement fund isn’t about deprivation; it’s about prioritizing freedom, health, and experiences over stuff. By planning ahead, living intentionally, and leveraging resources like Social Security, you can step into retirement confidently. It’s never too late to adjust—small changes today can lead to a rewarding tomorrow. Start reviewing your budget and goals now, and you’ll be amazed at what’s possible.